Advocacy News – April 14, 2023

The city of Detroit has faced challenges with property taxes. Even as values rise, Detroit has continued to face the lowest property values of any large city in the country, combined with one of the highest property tax rates. A variety of factors have created a negative cycle that the municipality is looking to break.

For Detroit leaders, based on a study by researchers at the Lincoln Institute for Land Policy, a “split property tax” may help their municipality tackle this issue and that could be a benefit and available to other cities as well.

This week, city and Institute representatives met virtually with one of the Michigan Chamber’s key internal policy committees – our Tax Policy and Economic Competitiveness Committee – comprised of members from across the state to present the idea and answer questions.

What is Split-Rate Property Taxation?

The concept centers on taxing land at a different rate than the building on the property by decreasing or removing certain local millages and replacing it with a tax on the market value of the land. The idea is to reduce the cost of improvements and incentivize development while increasing the cost on speculators simply holding vacant land.

Proponents say there would not be an increase in local taxing authority and that it would still require local authorization, keeping the state’s Headlee Amendment intact, a 1978 voter-approved constitutional amendment which capped the amount of property taxes that could be collected by a local jurisdiction and adjust, or roll-back, the rate according to inflation. As outlined in the proposal: “Under the 1978 Headlee Amendment, increases in property tax collections beyond the rate of inflation trigger a rollback of the millage rate…Instead of rolling back millages, local governments, could elect to reduce taxes assigned to nonland property forms. This allows local governments to convert a statutory constraint into better market outcomes.” It is also believed that this change would not conflict with the Michigan Constitution as it would require a local vote and opt-in process.

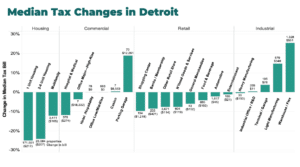

How Would it Work in Detroit, Other Municipalities?

How the proposed structure affects Detroit businesses is highlighted below, per the proposal:

The proposal as envisioned currently is not a Detroit-specific option, but could be available to every municipality as there would be a local vote to “opt-in” to this split property rate.

What’s Next?

No formal legislation to incorporate this policy has been introduced at this point and the Michigan Chamber has not yet taken a position.

The Chamber’s Tax Policy & Economic Competitiveness Committee and business advocacy team are studying and analyzing the proposal in greater detail and to ensure key components and potential ramifications are fully understood.

We’re also soliciting feedback from you, our member employers! Let us know your questions and how you believe this may affect your business and industry, or help or hurt your operations.

Please reach out to Leah Robinson at lrobinson@michamber.com with questions, for more information and to share your comments – or if you are interested in joining the Chamber’s policy committee on these matters.

To read the entire split-property tax proposal and to learn how the city of Detroit and Lincoln Institute partners believe it could be a successful strategy in Michigan, and how it might affect your industry, click here.