Advocacy News – November 2, 2021

Last week, President Biden revealed a new framework for the Build Back Better Act (BBBA) legislation creating the next congressional budget. Scaling back from the original $3.5 trillion price tag, the revised framework supposedly costs approximately $1.8 trillion, which the Biden Administration claims is entirely paid for under the BBBA. However, that cost has yet to be confirmed by the Congressional Budget Office (CBO). Despite a lack of concrete data regarding the costs of the BBBA, the U.S. House Ways and Means Committee is slated to vote on the bill as early as this week. So, what’s new? What remained? And why does it matter for Michigan’s businesses?

President Biden has emphatically stated taxing high-income earners is a fair and just approach to leveling the playing field in the United States. However, his BBBA framework affects all taxpaying Americans, no matter the income level. Hiking up tax rates discourages investments in Michigan’s businesses, results in lower wages for employees and ultimately stifles a recovering economy. The Biden Administration’s framework implies that businesses and their owners should be punished for success. For Michigan’s high-income earners, the BBBA imposes a combined 58.1% income tax rate, with the lowest top marginal tax rate of 51.4% in 8 other states, including Tennessee. The proposed BBBA framework encourages businesses and their investments to flock to states with a lower tax rate, and in turn, crushes Michigan’s competitiveness. Under the plan, the average top marginal tax rate across the U.S. would be 57.4%. The status of additional provisions is outlined below.

Updated:

- Capital Gains Tax: The increase in capital gains tax, included in previous versions of the BBBA, was not included in the most recent iteration, which will likely provide some relief to businesses. However, according to public accounting and business advocacy firm, Plante Moran, individual taxpayers would be subject to a 5% surcharge on modified adjusted gross income (MAGI) in excess of $10 million and an additional 3% surcharge on MAGI in excess of $25 million. Those thresholds are reduced by 50% for married taxpayers filing separately (e.g., $5 million and $12.5 million). Estates and trusts would be subject to much lower thresholds of $200,000 and $500,000 of MAGI. Since the tax surcharge is levied on MAGI, it will apply to all types of income and will increase the effective tax rate applicable to capital gains, dividends and ordinary income for applicable taxpayers.

Not included:

- State and Local Tax (SALT) Cap Repeal: Although not included in the latest version, Congressional Democrats still seem to be weighing the possibility of inclusion, as it predominately benefits blue states. However, it has been argued that repealing the SALT cap would also provide high-income earners with a tax cut incentivizing Democrats to hold off for now.

- Qualified Business Income Deduction (QBID): In previous versions of the BBBA, the House Ways and Means Committee pushed to speed up the sunset of a provision which allowed certain businesses to deduct 20% of income from federal tax to January 1, 2022. The latest iteration did not include the provision, meaning the sunset of 2025, created by the 2017 Tax Cuts and Jobs Act, is still in place.

- Estate and Gift Tax: Due to an uproar of hardworking Americans and their life-long investments, changes in the estate and gift tax laws, previously included in the BBBA, have been removed.

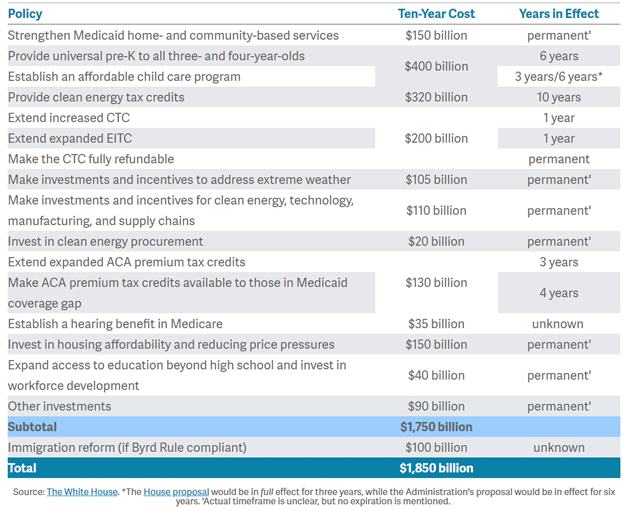

For a broader look at the BBBA and what the supposed $1.8 trillion will be funding, see below for a breakdown provided by the White House:

To oppose the BBBA, please make your voice heard by reaching out to Congressman Dan Kildee here. Congressman Kildee is Michigan’s only Congressional representation on the U.S. House Ways and Means Committee.

For more information, please contact Leah Robinson at LRobinson@michamber.com.